Dublin, Sept. 29, 2022 (GLOBE NEWSWIRE) — The “Bone Allografts Market Size, Share & Trends Analysis Report by Application (Dental, Spine), by End-use (Hospitals & Dental Clinics, Orthopedic & Trauma Centers) by Type (Cancellous, Cortical), and Segment Forecasts, 2022-2030” report has been added to ResearchAndMarkets.com’s offering.

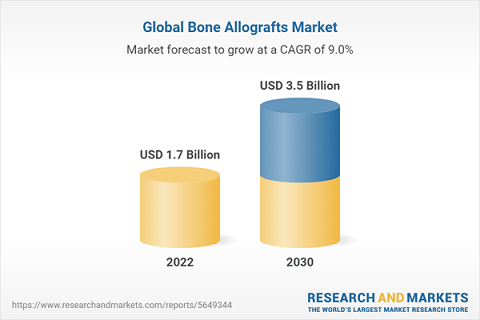

The global bone allografts market size is anticipated to reach USD 3.5 billion by 2030, according to this report. The industry is expected to expand at a lucrative CAGR of 9.0% from 2022 to 2030. The rising prevalence of dental problems, ongoing product commercialization, market accessibility & product affordability, rising elderly population, and increasing public awareness regarding preventative care are the major factors driving the demand for dental bone allografts.

For instance, about 530 million children experience caries of their primary teeth, according to the World Health Organization (2020), which estimates that nearly 3.5 billion people are affected by oral disorders. Furthermore, the growing demand for minimally-invasive procedures will also support market growth.

As Minimally Invasive Spine Surgery (MISS) does not require a big incision, it reduces the risk of major injury to the muscles surrounding the spine and allows the surgeon to see only the area of the spine where the problem arises. Due to these approaches, such as using fewer devices, the surgical field (also known as exposure) is smaller, resulting in less pain and a speedier recovery.

These factors are expected to drive the overall industry. The industry had a decline in 2020 as a result of the COVID-19 pandemic. All elective surgeries, including spine surgery, were postponed between March 17 and June 8, 2020, and the hospitals were transformed into recognized COVID-19 treatment facilities. Such elements consequently hampered the industry expansion.

The expansion of treatment access in many developing countries is likely to increase demand for healthcare-related products, notably those connected to spinal surgery. The market would expand as a result of the rising demand for these goods as major developing regions’ economies became more prosperous.

Furthermore, due to the temporary shutdown of dental clinics and the fact that all healthcare providers were occupied with COVID-19, dental procedure volumes were substantially decreased. Access was limited to only the most basic care. For instance, the American Dental Association (ADA) advised delaying elective dental surgeries until April 6, 2020, and dental offices should only offer emergency dental care. These factors severely impacted the supply chains of dental bone graft substitute producers.

Thus, these data suggest that during the COVID-19 pandemic, the demand for dental bone graft alternatives decreased. In dentistry, bone allografts are frequently used. A skilled clinician who can handle and position the allografts in the proper position is required for the preparation and processing for safe use and successful transplant material.

The materials’ antigenicity and danger of disease transfer from donor to the recipient are the main issues. Other bone-related operations, from small flaws to significant bone loss following tumor removal, also use bone allografts. Furthermore, the increasing medical and dental tourism sector, burden of dental illnesses, and technical developments in the field of dentistry are also among the key factors contributing to the industry growth.

Bone Allografts Market Report Highlights

- An increasing number of sports & trauma injury cases and orthopedic surgeries performed is expected to boost the industry growth

- The demineralized bone matrices type segment dominated the industry in 2021 owing to a high number of spinal fusion and dental surgeries performed

- The dental application segment held the largest share of the overall revenue in 2021 and is also expected to register the highest CAGR over the forecast period

- To replace missing teeth, bone grafting is done first. Bone grafts are additionally utilized in dentistry as fillers and scaffolds to enhance bone growth & accelerate wound healing, which is expected to propel the segment growth

- The hospitals & dental clinics end-use segment held the largest market share in 2021 due to the availability of technologically sophisticated implants for treating and diagnosing spine problems

Key Topics Covered:

Chapter 1 Research Methodology & Scope

Chapter 2 Executive Summary

Chapter 3 Bone Allograft Market Variables, Trends & Scope

3.1 Market Lineage Outlook

3.1.1 Parent Market Analysis

3.1.2 Ancillary Market Analysis

3.2 Penetration & Growth Prospect Mapping

3.3 Bone Allograft Market Dynamics

3.3.1 Market Driver Analysis

3.3.1.1 Growing adoption of minimally invasive surgeries

3.3.1.2 Increasing Geriatric Population

3.3.2 Market Restraint Analysis

3.3.2.1 High Costs And Risks Associated With Surgery

3.4 Bone Allograft Market Analysis Tools: Porters

3.4.1 Bargaining Power Of Suppliers: Moderate To High

3.4.2 Bargaining Power Of Buyers: Moderate

3.4.3 Threat Of Substitutes: Moderate To High

3.4.4 Threat Of New Entrants: Low

3.4.5 Competitive Rivalry: Moderate To High

3.5 PESTLE Analysis (Political & Legal, Economic, Social, Technological, and Environmental Landscape)

3.6 Regulatory Framework

3.7 Key Opportunity Analysis

3.8 Pricing Analysis

3.9 Technology Trends Analysis Technology Overview (Emerging Trend Analysis)

3.10. COVID-19 Impact Analysis

3.11 Investment Opportunity Analysis

Chapter 4 Bone Allograft Market: Competitive Analysis

4.1 Market Participation Categorization

4.2 Public Companies

4.2.1 Company Market Position Analysis

4.2.2 Synergy Analysis: Major Deals & Strategic Alliances

Chapter 5 Bone Allograft Market: Type Estimates & Trend Analysis

5.1 Type Market Share Analysis, 2021 & 2030

5.2 Type Dashboard

5.2.1 Cortical Bone Allografts

5.2.2.1 Cortical Bone Allografts market estimates and forecasts, 2017 – 2030 (USD Million)

5.2.3 Cancellous Bone Allografts

5.2.3.1 Cancellous Bone Allografts market estimates and forecasts, 2017 – 2030 (USD Million)

5.2.4 Corticocancellous Bone Allografts

5.2.4.1 Corticocancellous Bone Allografts market estimates and forecasts, 2017 – 2030 (USD Million)

5.2.5 Demineralized Bone Matrices

5.2.5.1. Demineralized Bone Matrices market estimates and forecasts, 2017 – 2030 (USD Million)

Chapter 6 Bone Allograft Market: Application Estimates & Trend Analysis

6.1 Application Market Share Analysis, 2021 & 2030

6.2 Application Dashboard

6.2.1 Dental

6.2.1.1 Dental market estimates and forecasts, 2017 – 2030 (USD Million)

6.2.2 Spine

6.2.2.1 Spine market estimates and forecasts, 2017 – 2030 (USD Million)

6.2.3 Reconstruction & Traumatology

6.2.3.1 Reconstruction & Traumatology market estimates and forecasts, 2017 – 2030 (USD Million)

6.2.4 Others

6.2.4.1 Others market estimates and forecasts, 2017 – 2030 (USD Million)

Chapter 7 Bone Allograft Market: End-Use Estimates & Trend Analysis

7.1 End-Use Market Share Analysis, 2021 & 2030

7.2 End-Use Dashboard

7.2.1 Hospitals & Dental Clinics

7.2.1.1 Hospitals & Dental Clinics market estimates and forecasts, 2017 – 2030 (USD Million)

7.2.2 Orthopedics And Trauma Centers

7.2.2.1 Orthopedics and trauma centers market estimates and forecasts, 2017 – 2030 (USD Million)

7.2.3 OTHERS

7.2.3.1 Others market estimates and forecasts, 2017 – 2030 (USD Million)

Chapter 8 Bone Allograft Market: Regional Estimates & Trend Analysis, by Type, Application and End-Use

Chapter 9 Company Profiles

9.1 MEDTRONIC

9.1.1 Company Overview

9.1.2 Financial Performance

9.1.3 Product Benchmarking

9.1.4 Strategic Initiatives

9.2 DePuy Synthes (Johnson & Johnson Services Inc.)

9.2.1 Company Overview

9.2.2 Financial Performance

9.2.3 Product Benchmarking

9.2.4 Strategic Initiatives

9.3 Zimmer Biomet

9.3.1 Company Overview

9.3.2 Financial Performance

9.3.3 Product Benchmarking

9.3.4 Strategic Initiatives

9.4 Stryker

9.4.1 Company Overview

9.4.2 Financial Performance

9.4.3 Product Benchmarking

9.4.4 Strategic Initiatives

9.5 Lynch Biologics, LLC

9.5.1 Company Overview

9.5.2 Financial Performance

9.5.3 Product Benchmarking

9.5.4 Strategic Initiatives

9.6 Biomatlante

9.6.1 Company Overview

9.6.2 Financial Performance

9.6.3 Product Benchmarking

9.6.4 Strategic Initiatives

9.7 Royal Biologics.

9.7.1 Company Overview

9.7.2 Financial Performance

9.7.3 Product Benchmarking

9.7.4 Strategic Initiatives

9.8 Smith & Nephew.

9.8.1 Company Overview

9.8.2 Product Benchmarking

9.8.3 Strategic Initiatives

9.9 Xtant Medical

9.9.1 Company Overview

9.9.2 Financial Performance

9.9.3 Product Benchmarking

9.10 Baxter

9.10.1 Company Overview

9.10.2 Product Benchmarking

For more information about this report visit https://www.researchandmarkets.com/r/3ruo3a